During the liquidity crisis of Q1 25YO, where did on-chain transaction volume flow to?

Original Article Title: Where is Onchain Volume Rotating? (Jan 24-Mar 25)

Original Article Author: @stacy_muur, CuratedCrypt0 Member

Original Article Translation: Motion小Deep

Editor's Note: From January 2024 to March 2025, DeFi on-chain transaction volume experienced a surge and downturn. DEX trading volume reached a peak of $380 billion in January 2025, followed by a 35% decline. Solana's native DEX emerged, holding 5 out of the top 10 seats, with Hyperliquid occupying over 60% of the perpetual contract market share. Leading DEXs such as Uniswap and PancakeSwap dominated around 40% of the trading volume. Chain-level market share saw fluctuations, with Solana, Ethereum, and Base showing varying degrees of persistence, while CEX still accounted for nearly 80% of spot trading. The future of DeFi depends on the chain that can solidify user habits, rather than mere speculation.

The following is the original content (restructured for easier reading comprehension):

Over the past 15 months, the DeFi liquidity landscape has been redrawn among different chains, moving away from hype-driven outliers and quietly concentrating on fundamentals rather than noise.

TL;DR

· DEX trading volume hit a historic high of $380 billion in January 2025, followed by a 35% drop in the next two months, signaling a possible short-term top.

· The top 10 DEXs now account for nearly 80% of the activity volume; Uniswap and PancakeSwap alone represent around 40%.

· Solana's native DEX quietly took the top spot, with 5 out of the top 10, and its share expanded due to meme-driven trading volume growth.

· Hyperliquid disrupted the perpetual contract landscape, rising from a newcomer to dominating over 60% of the market share by March 2025.

All insights are based on public data. Special thanks to DefiLlama for consistently providing high-quality statistical data.

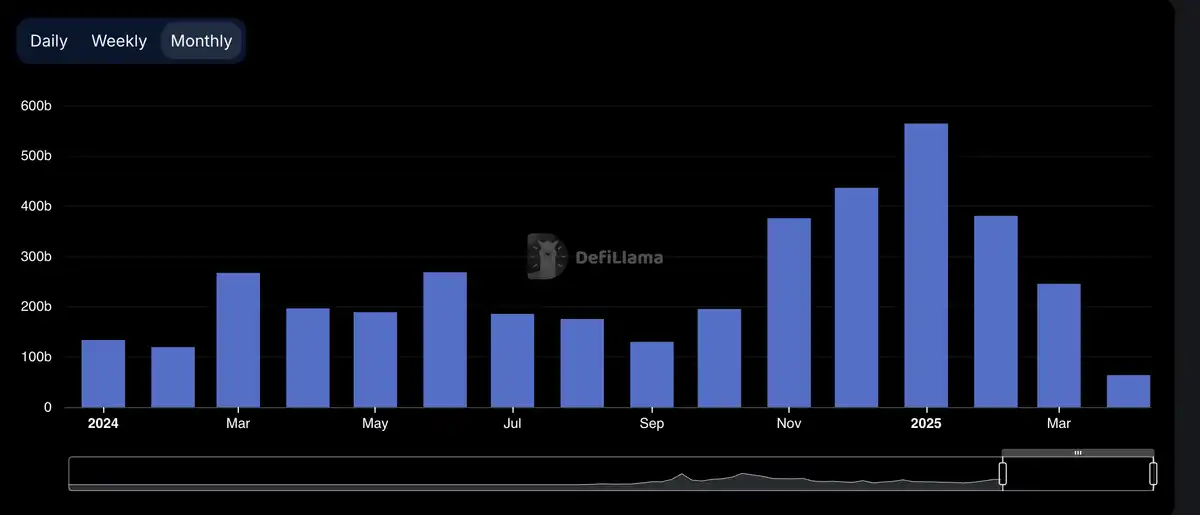

A Cycle Defined by Surges and Slowdowns

In early 2024, DEX trading volume showed strength in March and May, followed by a slowdown in the middle of the year.

The situation took a sharp turn in the fourth quarter, with transaction volumes surging in November and December, continuing into January 2025 to reach an explosive peak of $380 billion.

However, this wave of growth was short-lived. By February, the transaction volume had dropped to $245 billion, a steep 35% decrease, bringing an end to the three-month vertical climb. This decline set the tone for a more cautious second quarter.

DEX Dominance: Top Heavy Control

The DEX landscape remains highly concentrated. The top 10 protocols now account for 79.5% of daily trading volume, with just the top 5 controlling 59.1%.

Uniswap and PancakeSwap represent around 40% of all DEX trading volume, being the only two protocols with total trading volume exceeding a trillion dollars. Their dominance is built on first-mover advantage, cross-chain coverage, and deep liquidity.

Uniswap Labs has also launched Unichain, a dedicated Ethereum L2 based on the Optimism Superchain, aiming to provide fast, low-cost transactions with native cross-chain interoperability.

Solana's Quiet Rise

Solana's rise has been noteworthy. Five out of the top 10 DEXs are Solana-native: @orca_so, @MeteoraAG, @RaydiumProtocol, @Lifinity_IO, @pumpdotfun.

Orca (8.02%) and Meteora (6.70%) alone contribute about 15% of global DEX activity.

This rise is driven by low fees, fast block times, and the sticky flow of Solana's meme coin culture. Pump.fun entering the top 10 clearly reflects this energy.

Emerging Protocols: Fluid and Aerodrome

@0xfluid (7.09%) is the most capital-efficient DEX in the top 5. Active on Ethereum, with monthly trading volumes surpassing $100 billion. Its launch on Arbitrum saw volumes grow from $426 million in February to $1.6 billion in March, demonstrating rapid adoption.

@AerodromeFi, based on Base, reflects the growth of liquidity on the Base L2.

While Hyperliquid doesn't rank high in spot trading, it dominates the perpetual contract market with over 60% market share.

Chain-Specific DEX Market Share: Momentum Easy Come, Retention Rare

The past 15 months have shown that while most chains can attract attention, few can retain users. From January 2024 to March 2025, chain-level DEX market share has shifted rapidly, with only a few maintaining significant traction.

Solana has seen the most prominent performance. It steadily climbed in 2024, reaching a peak of 45.8% in January 2025 during the $TRUMP and $MELANIA meme coin craze. By March, its share halved to 21.5%. Nonetheless, its average share of 25.1% remains the highest across all chains.

Ethereum, on the other hand, exhibited the opposite trend. Starting at about 32% share in 2024, it dropped to 15.3% in January 2025 but rebounded to 26.4% by March, demonstrating its resilience even after losing momentum.

Base has been the most stable climber. Rising from 3% in March 2024 to 12.4% in December and remaining steady at 7.4% in March 2025, averaging 6.6% during this period. No hype, just gradual, sticky growth.

The BNB chain maintained an average share of 14.7%, remaining stable throughout, without any sudden spikes or crashes, sustained only by retail traffic, lacking any breakthrough moments.

Arbitrum started strong at 16% but failed to take off. By January 2025, it slipped to 4.8%, surpassed by Base and Solana.

Blast peaked at 42.3% in June 2024, only to vanish the following month—a typical case of incentive-driven transaction volume with no retention.

Conclusion: Chain-level DEX dominance is highly volatile. Solana surged, Ethereum recovered, Base slowly gained ground, and hype cycles quickly burned out. The enduring chains are not the loudest but the most utilized.

CEX Still Dominates Spot Trading Volume

Despite the DEX explosion at the beginning of 2025, centralized exchanges (CEX) continue to dominate the spot market. Even at the peak of DEX in January, CEX still held nearly 80% of the total trading volume.

While the CEX dominance dropped from 90% at the beginning of 2024 to a low of 79%, the overall pattern is clear: DEX is growing, but CEX remains the default venue for most traders.

Perpetual Contract Protocol Market Share

In 2024, the on-chain perpetual contract landscape saw a reversal.

After dYdX's two-plus-year reign at the top, Hyperliquid rose to redefine the dominant position. It first took the lead in February, briefly lost to @SynFuturesDefi mid-year, regained the top spot in August, and has held it since. By March 2025, Hyperliquid held nearly 59% of the perpetual contract trading volume, establishing itself as the preferred venue for professional traders.

This rise to prominence was fueled by a product offering close to a CEX experience, gaining attention. In contrast, dYdX quickly declined. Its market share dropped from 13.2% at the beginning of 2024 to 2.7% in March 2025 as users gravitated towards faster, sleeker, and more modern alternatives.

@JupiterExchange took a different path in perpetual contracts, climbing to second place with an 8.8% share by leveraging Solana-native liquidity and a spot DEX funnel. It expanded rapidly but stabilized behind Hyperliquid. Others such as SynFutures, @Vertex_Protocol, and @ParadexApp briefly showed traction.

Perpetual Contract Chains: The Execution Layer Rewritten in One Cycle

The most significant shift in perpetual contract infrastructure over the past year has not been in user preferences for a particular protocol but in their trust in which chain executes transactions.

In January 2024, Ethereum and Arbitrum controlled over 65% of the perpetual contract trading volume. However, by March 2025, this had plummeted to just 11.8%, overtaken by updated, faster execution layers.

Leading this transition is Hyperliquid's custom chain, which saw its share increase from 13.6% to 58.9% during the same period. In less than a year, it has become the default perpetual contract execution environment, supplanting the L1 and L2 layers that once defined the category. Not only is it faster, but it also provides the high reliability and low latency that professional traders require.

Solana also showed strength, rising to nearly 16% by the end of 2024 with Jupiter and Phoenix, but eventually stabilizing at 10-11%, failing to sustain its breakout momentum. Base and ZKsync showed vitality, peaking at around 6-7%, but have not yet reached the top tier.

Meanwhile, Blast became a cautionary tale: achieving a 18.8% single-month miracle in June 2024, only to quickly vanish. In the realm driven by product quality and user retention, hype failed to endure. The new execution stack is clear—performance-first chains have reset the standard, and traditional infrastructure is no longer the default choice.

The future of DeFi lies not in the number of chains, but in solidifying the narrative into user habits.

You may also like

Morning Report | OpenAI has submitted an S-1 registration statement draft to the U.S. SEC; Morpho completes $175 million financing

Galaxy Deep Research Report: How Hyperliquid's HIP-4 Upgrade Changes the Landscape of Prediction Markets?

Latest research from 13 top universities including Cornell University: The current state, challenges, and misconceptions of the fusion of Crypto and AI

Deconstructing Anthropic: The Best AI Company, Possibly Also a Type of Organizational Invention

Every exchange is a "Universal Exchange."

The counterattack of traditional finance: Alliance chains are quietly reviving

Pantera Capital Partner: How Tokenization is Restructuring the Private Equity and Early Investment Ecosystem?

Mastercard Launches Agent Pay for AI, Plans to Record AI Agent Payment Authorizations on Polygon

Mastercard launched Agent Pay for AI, a new payment protocol designed to help AI agents make small payments such as pay-per-use access to data and APIs. The system plans to record human-granted AI agent permissions on Polygon, focusing on verifiable authorization, identity, and payment controls.

Curve Deploys Llamalend v2 on Optimism With 250,000 OP Incentives

Curve launched Llamalend v2 on Optimism with 250,000 OP incentives from the Optimism Foundation. The upgrade expands Llamalend beyond its earlier crvUSD-focused model, adding broader collateral support, LlamaRisk market reviews, and the ability to use Curve LP tokens as collateral.

Raydium Old Liquidity Pool Reportedly Exploited, With $1.34 Million Moved to Ethereum and Tornado Cash

An old Raydium liquidity pool was reportedly exploited for around $1.34 million in USDC, RAY, and wSOL, with the stolen funds bridged to Ethereum and deposited into Tornado Cash. The incident highlights the tail risks of legacy DeFi pools, old contracts, and cross-chain fund laundering paths.

Kalshi Executive Challenges “SBF Backed AI Unicorns” Narrative, Says Leopold Aschenbrenner Was Key Figure

Kalshi executive John Wang questioned the “SBF backed AI unicorns” narrative, saying Leopold Aschenbrenner was the key figure behind major AI investment decisions.

New York Proposes Stricter Stablecoin Issuer Rules Aligned With Federal GENIUS Act

NYDFS proposed stricter stablecoin issuer rules aligned with the GENIUS Act, covering reserves, custody, redemption timelines, audits, and capital buffers.

CryptoQuant Says Bitcoin Profitable Supply Is Near 45% Pressure Zone as On-Chain Data Points to Market Repricing

CryptoQuant said Bitcoin’s profitable supply is nearing the 45% pressure zone, signaling rising market stress, unrealized losses, and a possible on-chain repricing phase.

Bitcoin Falls Below 200-Week Moving Average as On-Chain Data Shows Over Half of Supply in Loss

Bitcoin dropped below its 200-week moving average as on-chain data showed over 50% of circulating supply is now in loss, signaling rising market stress.

CFTC Reportedly Plans New Prediction Market Rules Focused on Manipulation Risk and Public Interest Review

The CFTC is reportedly preparing new prediction market rules focused on manipulation risk, public interest review, and retail trader protections.

Meet the new WEEX trial fund—your gateway to greater profits

WEEX Labs Lands at Dutch Blockchain Week: A Disruptive Crypto × AI Conversation Sets Sail in Amsterdam

SK Hynix Reportedly Plans U.S. ADR Listing as Early as August, With SEC Approval Possible in Late June

SK Hynix may pursue a U.S. ADR listing as early as August, with SEC approval reportedly possible in late June amid strong AI chip supply chain demand.