I finished translating the Circle IPO prospectus, and it shows that executive compensation is increasing while the company's gross profit is decreasing.

The issuer of the world's second largest stablecoin USDC, Circle, has officially initiated its listing plan, preparing to debut on the New York Stock Exchange. On April 2, the company filed its Form S-1 with the SEC, taking the long-awaited first step towards an IPO. The S-1 filing did not specify a timeline for the IPO, but typically trading can commence within weeks after a company submits an S-1. According to the S-1 Registration Statement, JPMorgan and Citigroup will act as lead underwriters, with the market expecting Circle's valuation to potentially reach $5 billion, under the ticker symbol "CRCL." The prospectus indicates that Circle will issue an unspecified number of Class A common shares, while existing shareholders will also register to sell a portion of their holdings. The pricing range per share has not yet been determined. Proceeds from the sale of shares will go to Circle, with proceeds from shareholder sales not going to the company.

This marks Circle's second attempt at going public. At the end of 2022, it had tried to go public through a merger with a SPAC (Special Purpose Acquisition Company) but the deal fell through due to regulatory issues, resulting in a loss of over $44 million. Since then, Circle has adjusted its strategy, gradually moving closer to financial centers. Last year, it relocated its headquarters from Boston to One World Trade Center in New York, further integrating into the global financial core.

This time, Circle has chosen a delicate timing—the tech stocks have recently experienced significant volatility, and the Nasdaq index just had its worst quarter since the start of 2022. If successful, Circle will become, following Coinbase, another heavyweight cryptocurrency company to land on a major U.S. exchange, while also being the first stablecoin-listed company.

Business Model: A Stablecoin-Centric Ecosystem

Circle's story began in 2013 when it positioned itself as a company focused on Bitcoin-related businesses, aiming to make digital currency usage more convenient through technology. As the crypto market evolved, Circle seized a new opportunity in 2018—partnering with Coinbase to launch the U.S. dollar stablecoin USDC through the Centre consortium. USDC is a digital asset pegged 1:1 to the U.S. dollar, designed to provide stability and credibility for crypto transactions.

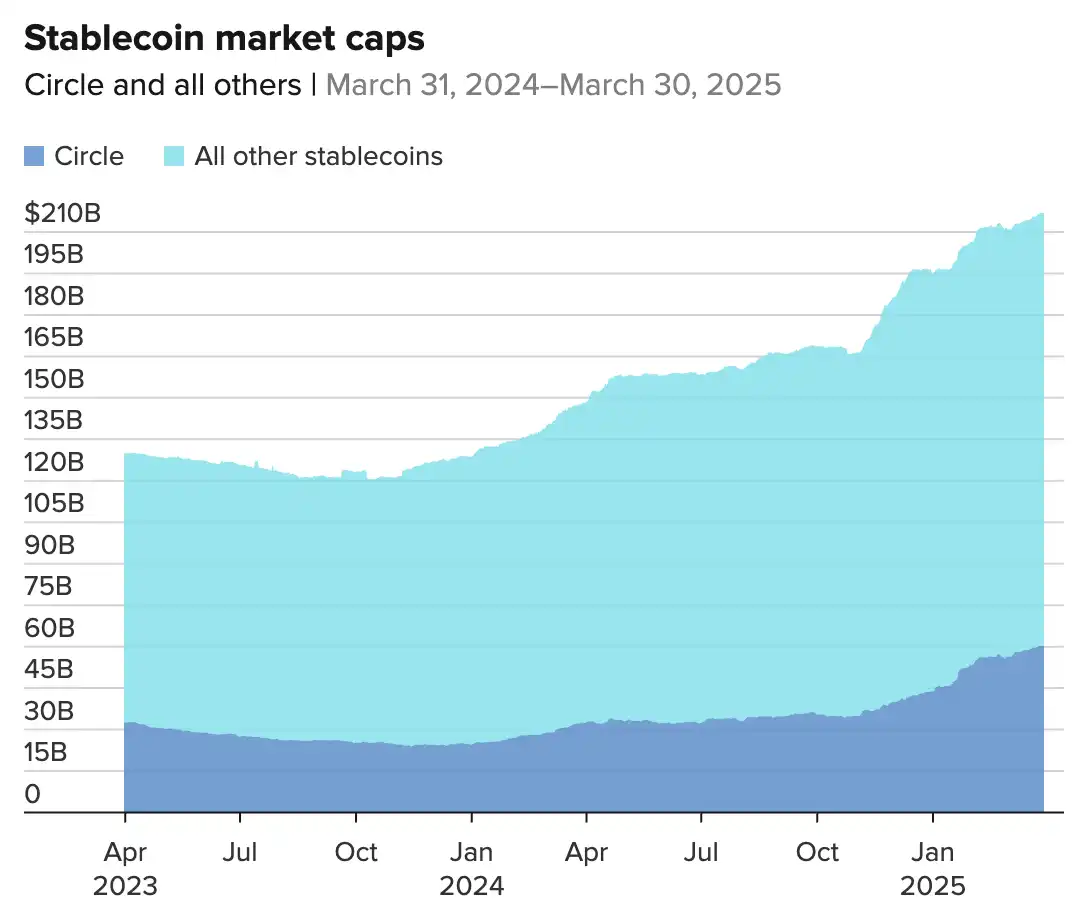

In 2023, the Centre consortium dissolved, granting Circle full control of USDC. Since then, USDC has evolved from a collaborative project into Circle's core asset. By 2025, USDC's market capitalization had reached $60.1 billion, trailing behind Tether's USDT (with a market cap of $144.4 billion), but its growth trajectory and transparency have secured its place in the market.

USDC is Circle's most well-known product, which is the world's second-largest stablecoin. During the last crypto bull run, USDC quickly rose to prominence, with its market cap skyrocketing from less than $1 billion in 2020 to over $500 billion in 2022, further growing to $601 billion in 2024, holding 26% of the entire stablecoin market. While the leader Tether (USDT) still maintains a commanding 67% market share, USDC has seen rapid growth this year — its market cap has grown by 36%, compared to Tether's mere 5%.

Data Source: CryptoQuant

Related Read: "Circle IPO Aims for $50 Billion Valuation, Is Stablecoin Going Public?"

Channel Distribution

Circle understands that the success of USDC relies on ecosystem support. Initially, it partnered with Coinbase to issue USDC through the Centre Consortium, but the consortium dissolved in 2023, and Circle took full control. As disclosed in the S-1, Coinbase now holds a minority stake in Circle, and both parties more evenly distribute profits based on the total reserve revenue (still divided based on the amount of USDC held in their respective wallets and custody products). In 2024, Circle earned approximately $1.7 billion in revenue and paid over $900 million to Coinbase as a distribution partner.

In December 2023, Circle partnered with the world's largest crypto exchange, Binance, agreeing to a one-time fee of $60.25 million and monthly proportional fees, allowing USDC to participate in the Binance Launchpool, leading to the USDC supply on the Binance platform increasing from under $1 billion to $4 billion.

This "spend to grow" strategy significantly increased the circulation and market recognition of USDC but also raised operational costs. Circle, through partnerships with giants like Coinbase, Binance, and BlackRock, built a robust distribution network, ensuring USDC's penetration in the global crypto ecosystem.

Ecosystem Expansion

The business model of Circle can be described as "Stablecoin + Ecosystem Expansion." It is not only a stablecoin issuer but also aims to build an ecosystem covering cryptocurrency payments, cross-chain technology, and even enterprise solutions through a series of products and services.

The issuance and circulation of USDC are at the core of Circle's business and its most important source of revenue. For each USDC issued, Circle deposits an equivalent amount of U.S. dollars or highly liquid assets in a bank as reserves to ensure its stability. Users can use USDC for transactions, payments, or storing value, while Circle earns revenue by managing these reserve assets. To expand the circulation of USDC, Circle has established deep partnerships with financial and crypto giants such as Coinbase, Binance, and BlackRock. For example, in the agreement with Coinbase, Circle sets a payment base rate based on the daily net income of USDC reserves, and after deducting a management fee, both parties share the proceeds proportionally. By 2024, the circulation of USDC has continued to grow, especially playing a significant role in the DeFi and cross-border payment fields.

In the realm of payments and enterprise services, Circle plays a bridging role between the crypto world and traditional business. It provides a complete set of payment APIs and enterprise tools that enable merchants to easily accept USDC payments and automatically convert them into fiat currency. This service model is similar to PayPal in traditional finance but optimized for the crypto economy. For example, an e-commerce platform can integrate Circle's Checkout service, and after consumers make payments with USDC, Circle will instantly convert the cryptocurrency to dollars and settle with the merchant, significantly reducing the barrier for businesses to enter the crypto payment space.

Cross-chain technology and blockchain infrastructure are another key barrier that Circle has built. The cross-chain bridge developed by the company allows USDC to freely move between different blockchains such as Ethereum and Solana, greatly enhancing the usability of the stablecoin. Additionally, the IPO prospectus revealed that Circle is developing a Layer 2 solution aimed at reducing transaction costs and improving efficiency, laying out its crypto infrastructure.

To more directly reach end-users, Circle has also launched digital wallet services. Although currently limited in scale, it is evident that the business is extending from B2B to B2C.

In summary, Circle's business model is like a "Stablecoin-Driven Ecosystem Loop": centered around USDC, it extends the potential of cryptocurrency to the real world through payments, technology, and user services. Its ambition is significant, covering nearly all crypto areas beyond CEX.

Financial Performance: Where Did Last Year's $1.68 Billion in Revenue Come From?

According to the prospectus, the financial data disclosed this time fully presented Circle's recent years' performance for the first time.

For the 2023 fiscal year (ending December 31), total revenue and reserve income reached $16.8 billion, a 16% year-on-year increase, continuing the growth from $14.5 billion in 2022 and $7.72 billion in 2021. Revenue in 2024 mainly came from interest income on reserve assets supporting USDC.

Total operating expenses in 2024 were $4.917 billion, with compensation expenses ($2.634 billion), general and administrative expenses ($1.373 billion), and IT infrastructure investment ($27.1 million) accounting for the majority. The net profit from continuing operations was $1.569 billion, lower than the $2.715 billion in 2023 but a significant improvement from the $7.618 billion loss in 2022. The 2024 adjusted EBITDA was $2.849 billion.

The company also recognized a $4.3 million impairment loss on digital assets for the year, while it gained $54.4 million in other income from non-core business activities. The prospectus has not yet finalized the weighted average number of shares outstanding or earnings per share data.

As per the plan, Circle intends to use the IPO proceeds for product development, working capital, scaling operations, and potential acquisitions, among other regular corporate purposes. A specific pricing timetable and share allocation plan have not been announced yet.

Operational and Financial Metrics

Circle earns money by managing the reserve assets of USDC. These reserves include cash and short-term U.S. Treasuries, generating significant interest income in a high-rate environment. The S-1 shows that for 2024, Circle's total revenue was $16.8 billion, with 99% (approximately $16.65 billion) coming from reserve income, while other sources (such as payment services and cross-chain technology) only contributed $15 million. This means that Circle is almost entirely reliant on a single source of revenue, which is also influenced by government interest rate policies. The filing estimates that a 1% interest rate decrease would reduce reserve income by $441 million. However, Circle believes that low rates may stimulate USDC circulation growth, but this relationship is "complex, uncertain, and unproven."

As of December 31, 2024, USDC has been used in approximately $20 trillion worth of on-chain transactions. The table below shows key operational and financial metrics during the period and the related GAAP (Generally Accepted Accounting Principles) metrics:

The USDC circulation and average USDC circulation are the main contributors to Circle's reserve revenue and are also metrics for measuring the breadth of the Circle stablecoin ecosystem. As of December 31, 2024, December 31, 2023, and December 31, 2022, the company held USDC amounts of $294.5 million, $275.8 million, and $5.3 million, respectively.

The Reserve Return Rate refers to the return rate generated by reserve assets and is a key determinant of reserve revenue. It is calculated as reserve revenue divided by the average period-end balance of the Circle stablecoin holder-exclusive reserve. As of December 31, 2024, December 31, 2023, and December 31, 2022, the company's Reserve Return Rates were 5.0%, 4.7%, and 1.5%, respectively.

Stablecoin Market Share refers to the percentage of circulating Circle stablecoins out of the total circulation of all fiat-backed stablecoins (i.e., digital assets pegged to the value of fiat currency). This metric reflects Circle stablecoin's share in the overall stablecoin market and its position in the competitive landscape. Since 2021, by circulation volume, Circle has been the world's second-largest stablecoin issuer. According to CoinMarketCap data, as of December 31, 2024, Circle's stablecoin market share was 24%.

Meaningful Wallets refer to the number of digital asset wallets with an on-chain USDC balance exceeding $10, serving as a key metric to gauge USDC adoption breadth. The number of Meaningful Wallets in 2024 was 4.26 million, representing a 53.24% increase from the end of 2023.

Profit Breakdown

The table below shows Circle's 2024 Income Statement, detailing the company's 2024 revenue, expenses, and net profit metrics:

As of December 31, 2024, the reserve revenue was $1.676 billion, a $230.5 million (16.1%) year-over-year increase compared to 2023. Of this, approximately $139.9 million of the growth came from the increase in average daily USDC balance in circulation, reflecting the growing demand for USDC associated with digital asset trading activity and Circle's market share gains in key markets; a $89.9 million increase came from the improvement in average yield, largely influenced by the Federal Reserve's interest rate hikes. Other income for 2024 decreased by $4.7 million (23.6%) year-over-year, primarily due to a $3.9 million decrease in transaction service revenue related to the gradual discontinuation of certain services in 2024.

In 2024, the annual distribution and transaction costs increased by $291 million (40.4%) compared to the end of 2023. The main reasons were a $216.6 million increase in distribution costs paid to Coinbase and an additional $74.1 million in other distribution incentives related to new strategic partnerships, such as a one-time prepaid fee to Binance. Other expenses for 2024 decreased by $1.4 million (17.2%) compared to 2023, primarily due to the company phasing out traditional transaction service products, resulting in a $0.9 million expense reduction.

The annual profit for 2024 was $156 million, a decrease of $112 million from the net income in 2023. Although the reserve income in 2024 increased by $230.5 million compared to 2023, the distribution and transaction costs also significantly increased by $291 million from the end of 2023, with total operating expenses increasing by $39 million, ultimately leading to a declining profit trend.

In terms of cash flow, for three consecutive years from 2022 to 2024, the USDC reserve cash balance held in bank accounts far exceeded the FDIC insurance limit of $250,000 per financial institution. As of December 31, 2024, approximately 85% of the USDC reserve was held in the Circle Reserve Fund, with the remaining portion held in cash in several bank accounts. The Circle Reserve Fund is managed by BlackRock. The fund is only available to Circle, and Circle is the sole shareholder of the Circle Reserve Fund.

Regarding financing, in 2024, the funds raised from financing amounted to $19.449 billion, while the funds raised in 2023 were -$20.322 billion. This was mainly due to the increase in circulating USDC in 2024, where stablecoin holder deposits' net change increased by $194.521 billion, whereas in 2023, there was a decrease in circulating USDC, resulting in a $203.222 billion decrease in stablecoin holder deposits' net change.

Shareholders and Executives: The Real Winners of the IPO?

Circle's IPO is not only about the company's future but also a capital feast. After going public, Circle will implement a three-class share structure: Class A shares issued in the IPO carry one vote per share; Class B shares held by co-founders Jeremy Allaire and Patrick Sean Neville carry five votes per share but do not exceed 30% of the total voting rights; Class C shares have no voting rights and may convert under specific conditions. Class B shares automatically convert to Class A shares when transferred outside approved channels.

In addition, according to the prospectus, CEO Jeremy Allaire's executive compensation includes a $900,000 annual salary, $9 million in stock awards, and an additional $2 million in benefits, totaling over $12 million. CFO Jeremy Fox-Geen's total compensation is $5.2 million ($500,000 in annual salary, $4 million in stock, and $700,000 in benefits). Other executives such as Chief Strategy Officer Elisabeth Carpenter, President and Chief Legal Officer Heath Tarbert, and Chief Product and Technology Officer Nikhil Chandhok have annual compensations ranging from $4 million to $5 million. Working at Circle evidently comes with generous rewards.

For venture capital giants, investors holding over 5% of the shares will make a substantial profit, including General Catalyst (the largest corporate shareholder), Beijing IDG Capital, Breyer Capital, Accel, Oak Investment Partners, and Fidelity. These institutions collectively hold over 130 million shares, and the IPO, valued between $4 billion and $5 billion, will bring them a significant return.

USDC's market capitalization has doubled in the past year, increasing from around $30 billion to $60 billion, but the market competition is intensifying. Primary competitor Tether (USDT) leads by a significant margin with a market cap of over $140 billion. Additionally, PayPal is set to launch its own stablecoin in 2023, and banking giants like JPMorgan are also exploring the blockchain field. In the S-1 filing, Circle lists these competitors, acknowledging the complex market environment.

Nevertheless, Circle remains optimistic about the future. The U.S. legislation regarding stablecoins is progressing rapidly, with the "GENIUS Act" and "STABLE Act" gaining attention. Bryan Steil, Chairman of the House Digital Asset Subcommittee, has stated that after the April 2nd deliberations, the two bills are expected to reach a consensus post-revision and are planned to be submitted for the president's signature within the first 100 days of the Trump administration. This development provides policy support to compliant stablecoin companies like Circle and signifies an increasingly clear regulatory framework for the U.S. digital dollar sector.

This IPO still needs to go through regulatory review and progress based on market conditions. Specific details such as the issuance size and per-share valuation will be disclosed through supplemental filings before the listing. While uncertainties remain, Circle's IPO is likely to become a key signal for the future direction of the stablecoin industry. With global regulatory policies becoming clearer, stablecoins are moving towards compliance and deeper institutional participation. Can Circle seize this opportunity, leverage the abundant capital flow from Wall Street into the crypto market, and challenge Tether's long-standing dominance? Facing multiple challenges in regulation, competition, and market volatility, can Circle meet market expectations? Only time will tell.

You may also like

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.